The process of establishing a new firm is exciting. There are numerous aspiring entrepreneurs who hope to create a new brand and become financially free. Nevertheless, the truth of the matter is that when it comes to running a company, one has to go through great obstacles and overcome various challenges that one might not know about. Knowing the real figures of the entrepreneurial endeavors can enable new start-ups take the right path.

The Reality of the First Few Years

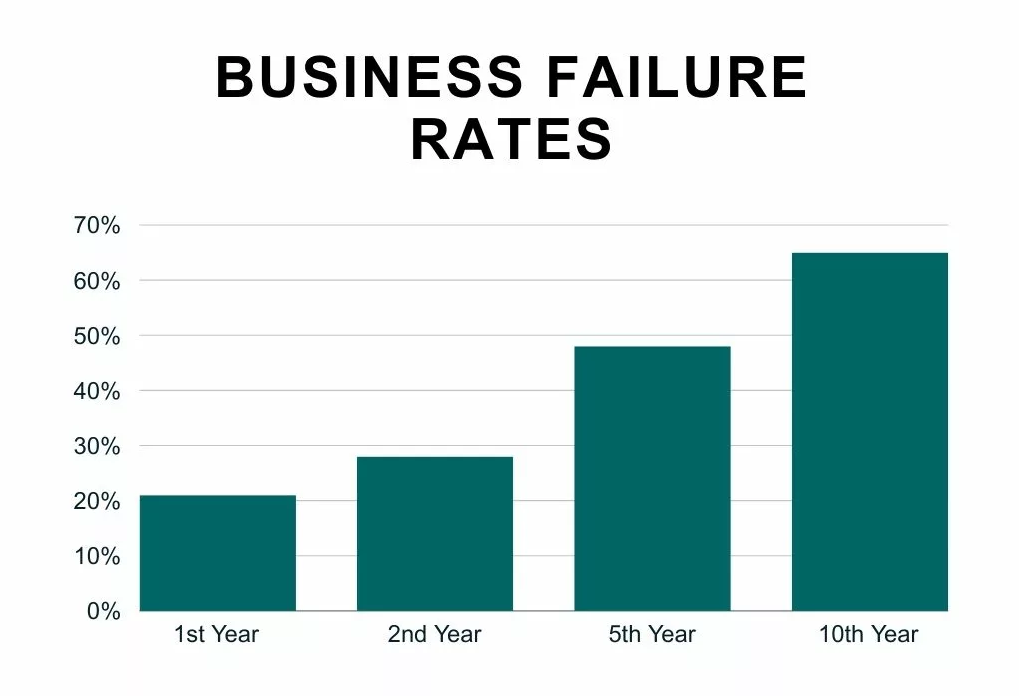

Start up is a period in which it is usually hard to maintain the business. The volume of work needed to keep the doors open is undermined by the many enthusiastic founders. A close examination of present day small business statistics will give a very clear display of these survival rates initially. The statistics indicate the presence of approximately twenty percent of new companies closing within the first twelve months of operation. With time, the survival rate keeps on decreasing very much. Being aware of these figures enables the new owners to remain fully-grounded and highly focused on their immediate daily objectives.

Possible Reasons Why New Ventures Do Not Succeed

Most businesses fail due to the mere reason that they have exhausted working capital too fast. This is a huge menace to any developing brand since it deals with poor cash flow management. The failure of other businesses is due to the fact that they make products where no one has the desire to purchase. Inability to appreciate the local market translates to un-moved stock and money that have been squandered. The other significant issue is the tendency to develop the team too rapidly when a company does not have a stable stream of revenue. It is much safer to remain small and highly flexible in the initial few years.

The Major Drivers of Long-Term Success

Those companies that make it in the tough early stages tend to have a number of similarities. There is no successful founder who does not have a very tight rein on his daily budgets. They also monitor each and every cost, and they do not waste money on luxuries in the office. Such winning brands are also keen to their core customers, and are always enhancing their daily services. The ability to create a highly committed customer base gives the chance to generate a reliable source of income. The other critical skill to ensure survival in the long run is the ability to adapt fast to the emerging market trends.

The Difference Planning Makes

An excellent plan is the most effective way of being resistant to unforeseen shifts. Business owners who will take the initiative to write a detailed operational plan have a high chance of survival. This is a cautious planning step, which makes founders reflect on whom they want to deal with and their key competitors. It, also, assists them in finding the required funding in local banks or private investors. With a roadmap, no one can make the mistake of doing something expensive, and all the staff is headed toward a common direction.

Conclusion

Entrepreneurship is a business adventure that one cannot be sure of and will not be fully risk-free. Although the failure rates may sound daunting initially they only show the high level of commitment needed to win. Through observing the pitfalls that other failed entrepreneurs get in to, new forms of entrepreneurs can find it easy to avoid those exact pitfalls. It is very long and very cunning day-to-day financial management to build a highly successful company. With the right information and a proper operation strategy every serious business person will create a successful brand that will endure.